Introduction to Cheque Dishonour and Legal Remedies in Bangladesh

This article will provide a comprehensive review of the issues surrounding cheque dishonour or cheque bounce in Bangladesh, including the legislation governing cheque dishonour, legal remedy for cheque dishonour, penalty, the liability of a loan guarantor in the event of a cheque bounce, and so on.

What exactly is a negotiating instrument?

A negotiable instrument is any document that guarantees the payment of money, either immediately or at a later date.

Negotiable Instrument Types:

Promissory Note:

A promissory note is a written instrument signed by the maker that contains an unconditional promise to pay a specified sum of money to a specific person or to the bearer of the instrument at a defined or determinable future period or on demand. The phrase ‘on demand’ refers to a note that is payable immediately or at sight.

Bill of Exchange:

a written instrument signed by the creator that contains an unconditional order directing a certain person to pay money to a certain person or to the bearer of the instrument at a definite or determinable time or on demand. Such instrument must have an order to accept or pay, and the direction/order must be accepted by the acceptor; otherwise, the instrument is not a bill of trade.

Cheque Dishonour and Cheque Bounce in BD

A bill of exchange is drawn on a particular banker and is only due on demand; it is issued for quick payment.

Cheque Dishonour

In simple words, a cheque bounce or dishonour occurs when a cheque cannot be honored and is returned by the bank due to insufficient funds.

However, in legal terms, it amounts to cheque dishonour when- a cheque drawn by a person on an account maintained by him with a banker for payment of money to another person from that account is returned by the bank unpaid, either due to insufficient funds or because the cheque exceeds the amount arranged to be paid from that account by an agreement made with that bank, then it amounts to cheque dishonour, which is an offence.

Furthermore, cheques may be returned for a variety of reasons, including-

- difference in amount between figure and word

- stale check undated/post-dated cheque, drawer’s signature differs/is missing, payment stopped by drawer,

- fraudulent endorsement account closed/dormant/blocked cheque not activated/intimation not received

- Cheque Dishonour Legal Framework

- Offenses involving cheque dishonour or cheque bounce are prosecuted in accordance with the terms of The

- Negotiable Instruments (N.I) Act 1881. This Act applies to the entire country of Bangladesh. The Act is regarded as a special law, and its provisions have precedence over any ordinary law.

Relevant law for Cheque Dishonour:

(i) What remedies are available for Cheque Dishonour?

In the event of a cheque being dishonored, the drawee may file a claim against the drawer. The plaintiff must determine where to bring a case for cheque dishonour. A Cognizance Magistrate Court must hear the case. The bank branch where the disputed cheque was submitted must come under the jurisdiction of that Court.

(ii) Procedure for Filing a Case Under Section 138 of the NI Act

The following elements must be met in order to launch a case for cheque dishonour under sections 138 and 140 of the N. I Act:

Step One:

The cheque must be handed to the bank within 6 months of its issuance or during the validity period. Furthermore, it can be presented to the bank as many times as the drawer advises the payee.

Step Two:

Within 30 days of the cheque being returned/dishonoured, a written notice must be delivered to the drawer of the cheque requesting payment.

Step three:

The drawer will have 30 days from the date of the notice to pay.

Step Four:

If the drawer fails to pay within the time specified, the drawee must file a case within 30 days of the expiration of the drawer’s payment deadline.

Claim Against Companies for Cheque Dishonour:

If a company commits an offence under section 138, the company and every person who was in control or responsible to the company at the time of the offence are liable for the offence under section 140 of the N. I Act.

Anyone who establishes that he had no knowledge of the offence being committed or that he took all reasonable means to prevent the commission of the offence is not responsible under section 140.

Serving a notice of dishonour on the firm will enough for a claim against a company; there is no requirement to serve notice on all partners implicated in the commission of the act.

Significant case law principles:

According to Shah Alam v State [63 DLR (2011) 137], if the drawer of the cheque has a malicious intent to dishonour the cheque, he is responsible under section 138 of the N.I Act.

In FaridulAlam v State [16 BLT (AD) 2008, it was found that if a person issues a cheque knowing that there is insufficient funds in the account, he is liable and prosecuted under Section 138 of the N. I Act. In Ahmed Lal Mia v State [66 DLR (AD) 204] and SM Redwan v Md. Rezaul Islam [66 DLR (AD) 169], a similar point of view was articulated.

In Khondokar Mahtabuddin Ahmed v State, the Supreme Court declared that there can be no legal impediment if a criminal charge is launched while a civil claim on the identical topic is proceeding before the court.

It is clear from the case of Anwarul Karim v Bangladesh that section 138 of the N. I Act has nothing to do with the recovery of the loan amount. The criminal case represents the offense, whereas the civil suit represents the monetary recovery.

The court concluded in AbulKalam Azad v State (Metro sessions Case No. 152 of 2007) that a single notification for numerous dishonoured cheques is not acceptable, and the norm has been deemed absolute.

In a recent decision on 17 February 2020, the Supreme Court’s Appellate Division stated that in order to impose culpability, a valid justification for acceptance of cheques must be shown. If the promise considered when issuing the cheque is not fulfilled, the cheque drawer is under no duty to pay the money to the cheque holder.

“Where the amount promised is contingent on some other complementary facts or the fulfillment of another promise, and if any cheque is issued on that basis, but that promise is not fulfilled, it will not create any obligation on the part of the drawer of the cheque or any right which can be claimed by the holder of the cheque,” the court stated.

As a result, in order to recover the sum pledged by the drawer in the cheque, the complainant must demonstrate consideration on his behalf.

Cheque Dishonour Punishment

Under the Negotiable Act of 1881, the offence is punishable by imprisonment for a term up to one year, a fine up to three times the value of the cheque, or both.

Limitations on filing an appeal

There shall be no appeal against a sentence order under section 138(1) unless the drawer deposits 50% or more of the dishonoured money before filing the appeal in the court granting the sentence.

What happens if the cheque’s drawer dies?

During the N. I case, the drawer dies:

The case is closed when the accused dies, and the complainant’s only option is to initiate a civil complaint against the accused’s legal heirs. This is because the case under Section 138 of the N. I Act is criminal in nature, and criminal obligation cannot be transferred to the accused person’s legal successors.

Drawer passes away during the appeals process:

If the drawer of the cheque dies while the appeal case is pending, the appeal (save for an appeal from a fine) will be dismissed. The complainant must file a civil court case in order to recover money under the sentence of a fine from the legal heirs of the deceased accused.

When the cheque is no longer valid, the following alternatives are available:

If a cheque is not given to the bank and is not dishonoured within the time stipulated in the statute, it becomes obsolete. When a cheque becomes obsolete and you are unable to file a complaint under the Negotiable Instruments Act 1881, you have four other options for seeking redress. In due order, the holder may take the following actions:

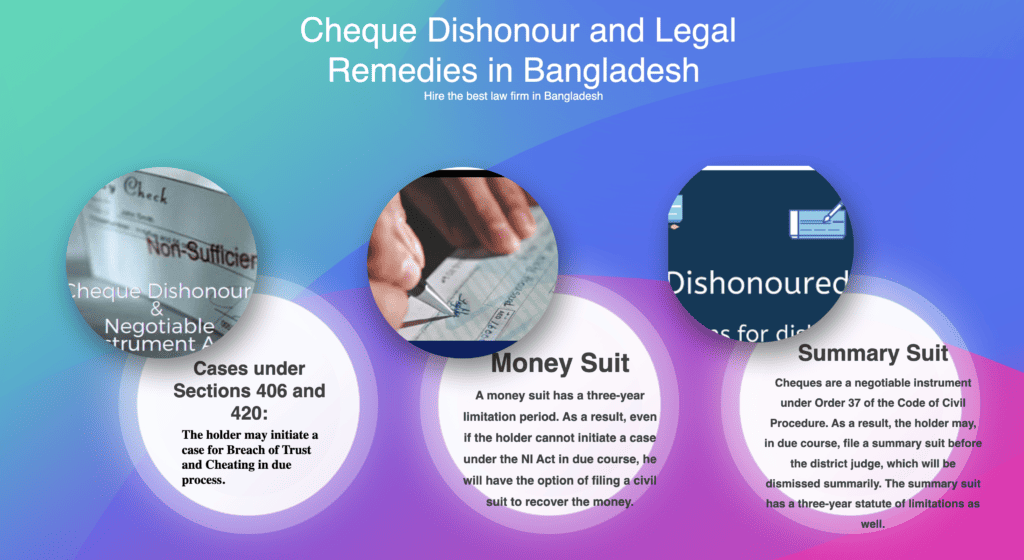

(i) Cases under Sections 406 and 420:

The holder may initiate a case for Breach of Trust and Cheating in due process.

(ii) Money Suit:

A money suit has a three-year limitation period. As a result, even if the holder cannot initiate a case under the NI Act in due course, he will have the option of filing a civil suit to recover the money.

(iii) Summary Suit:

Cheques are a negotiable instrument under Order 37 of the Code of Civil Procedure. As a result, the holder may, in due course, file a summary suit before the district judge, which will be dismissed summarily. The summary suit has a three-year statute of limitations as well.

Can a loan guarantor be held accountable for the dishonour of a check issued by the loanee?

At the moment of loan acceptance by the bank, one or more guarantors are required to accompany the borrower. It is a well-established legal principle that actions under Section 138 of the N.I Act cannot be taken against the guarantor for the dishonor of a cheque issued by the loanee.

However, he may be held civilly liable for the obligation he guaranteed; Hardeep Singh Nagra v State & another. If the borrower fails to pay back the loan, the guarantor will do so. If the guarantor issues a cheque to make such payment, he is liable under section 138 if the cheque is dishonoured on presentment for encashment.

Arbitration and Dishonour of Cheques:

Arbitration clauses in contracts:

Section 7 of the Arbitration Act 2001 states that whatever the current law in force directs, they will be treated as non-obstante clauses and the court shall not have jurisdiction to hear any other legal proceedings other than the provisions of the Arbitration Act 2001.

The Act of Negotiable Instruments of 1881 and the Arbitration Act of 2001:

The N. I Act and the Arbitration Act of 2001 are both exceptional legislation. The Act establishes provisions for instituting criminal prosecutions for offenses covered by this Act. Arbitration proceedings, on the other hand, are considered civil affairs.

Furthermore, according to customary law, if a conflict arises between ordinary law and special law, the special law shall always prevail unless stated otherwise; Hashmat Ullah v Azmir Bibi and others (44 DLR 332, 337), Managing Director, Rupali Bank and others v Tofazzal Hossain and others [44 DLR (AD) 260, 263].

“An arbitration clause does not cover a criminal proceeding,” asserts Probir Roy v State of West Bengal [II (1996) BC 308 (Cal). As a result, a criminal prosecution cannot be avoided on the basis of an arbitration agreement.”

According to Shahnewaz Akhan v The State and others [19 BLT (HCD) (20110 349], “there is no legal bar to filing a criminal case for criminal liability despite the fact that a civil suit is pending over the same matter.”Even if the agreement includes an arbitration clause, an aggrieved party may launch a criminal prosecution. Similar conclusions were reached by the court in Mohd. Majharul Hoque Monsur v Mir Kashim Chowdhury and others [2016 (2) LNJ 259, 261-262].

In the presence of an arbitration clause, the writ petition:

A party to an agreement may not bring a writ petition in the High Court Division if the agreement offers explicit directions for dispute resolution; Md. Mobarak Hossain v. The State and others [2011 (XIX) BLT (HCD) 54,60].

Case dismissed under Section 138 of the N. I. Act:

An arbitration proceeding is a civil procedure, and as such, it is not permissible to quash a prosecution under section 138 of the N.I Act because of the pendency of an arbitration hearing; Sri Krishna Agencies v State 2009 Cr LJ 787(SC).

Section 138, in conjunction with Section 7 of the Arbitration Act of 2001:

The High Court Division concluded in Mohammad Majharul Hoque Munsur v Mir Kashim that arbitration processes and section 138 prosecution can coexist without any legal impediment. [The State v. Shahnewaz Akhand, 19 BLT (HCD) 349].

In Khondokar Mahtabuddin Ahmed v State, the Supreme Court declared that there can be no legal impediment if a criminal case is launched while a civil complaint on the same topic is pending before the court. Section 138 of the N. I Act, as demonstrated in the case of Anwarul Karim v Bangladesh, has nothing to do with the recovery of the loan amount. The criminal case represents the offense, whereas the civil suit represents the monetary recovery.

Legal assistance in N. I Act cases Tahmidur Rahman Remura Wahid:

The Barristers, Advocates, and Lawyers at TRW law firm in New Mohakahli, Dhaka, Bangladesh have extensive expertise guiding clients through the whole process of litigation under the N. I Act in Bangladesh. For any questions or legal assistance, please contact us through email and phone at:

GLOBAL OFFICES:

DHAKA: House 410, ROAD 29, Mohakhali DOHS

DUBAI: Rolex Building, L-12 Sheikh Zayed Road

LONDON: 1156, St Giles Avenue, Dagenham

Email Addresses:

info@trfirm.com

info@tahmidur.com

info@tahmidurrahman.com

24/7 Contact Numbers, Even During Holidays:

+8801708000660

+8801847220062

+8801708080817